YOUR LOANS

The following are some of the programs that ABRA GROUP can offer. To be able to better understand your needs, please fill out the information by clicking the link below. An expert representative will contact you with a best avenue of approach.

There are two major types of mortgage loans: government-backed and conventional. Government-backed mortgage programs offer guarantees to lenders that reduce their risk and can make it easier for borrowers to qualify for a mortgage. Conventional loans do not offer the same guarantees but may have lower interest rates.

Here are some of the programs that are available:

ARM PROGRAM

Mortgage loans come in many varieties. One of them is the adjustable-rate mortgage. Commonly referred to as the ARM. Unlike a fixed-rate mortgage, in which the interest rate is locked in for the life of the loan, an ARM is a mortgage that has an interest rate that changes. An ARM might be a good option for someone who plans to sell or refinance within a few years because of the potential savings on interest charges early in the life of the loan. However, ARM is not the best choice for every borrower because of the potential rate increases over time. Because of their complexities, borrowers should fully understand the benefits and drawbacks of any ARM under consideration.

There are two major types of mortgage loans: government-backed and conventional. Government-backed mortgage programs offer guarantees to lenders that reduce their risk and can make it easier for borrowers to qualify for a mortgage. Conventional loans do not offer the same guarantees but may have lower interest rates.

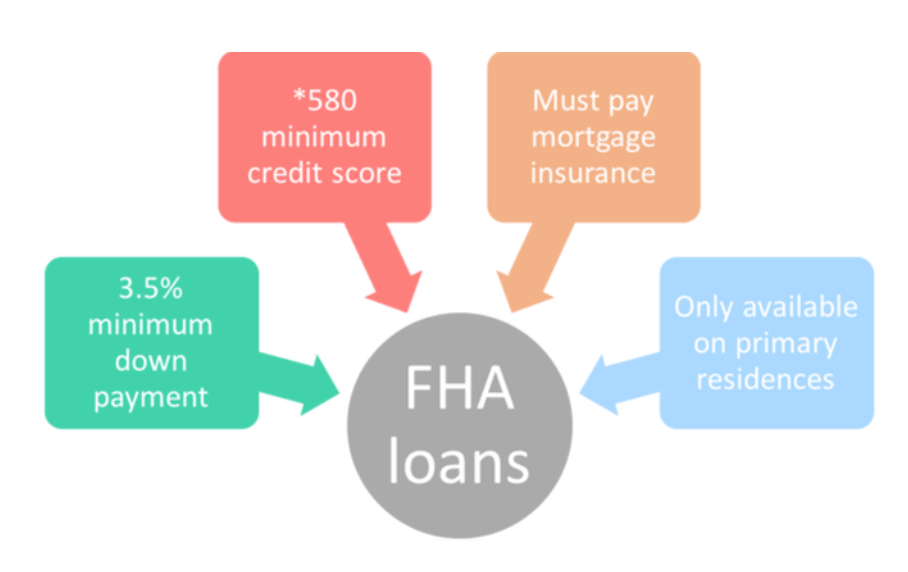

FHA LOANS

For most Americans, the purchase of a home is made possible with a mortgage. However, saving a 20 percent down payment is an unattainable goal for many potential buyers in areas with high home prices. Compounding the challenge are strict underwriting requirements, including some that were put into place to protect the housing market from a crash. Underwriting is the process mortgage lenders use to determine whether to approve a loan, based on the borrower’s risk profile.

The Federal Housing Administration, or FHA, loan program was created to help Americans buy homes following the Great Depression, and it remains a popular choice for people who need an affordable mortgage option. FHA loans are a popular solution because they allow for smaller down payments, while also resolving some of the underwriting challenges borrowers face. FHA mortgages are made by lenders and insured by the Federal Housing Administration, a U.S. government agency. With a government guarantee, the lender can offer more flexibility in its underwriting requirements including credit guidelines and the size of the down payment.

”If a borrower has good credit but limited cash on hand, other government-backed loans are available for less money down,” says Stephen Moye, senior loan officer for Citywide Home Loans. “For a borrower with a bankruptcy, foreclosure or other credit issue, the FHA loan has a much lower barrier to entry.”

HOME EQUITY LOANS

The major upside of homeownership is that instead of paying your landlord, your monthly payments help you build equity. Home equity is the value of how much of your property you actually own and is often a homeowner’s most valuable asset. If you need to borrow money against this asset, companies such as banks and credit unions will lend you money using your equity as collateral.

Homeowners tend to take out home equity loans to cover large expenses such as home repairs, home improvements and college tuition, as well as for purchasing a second home and consolidating high-interest loans. In those scenarios, a home equity loan may be a good solution, but there are also risks involved.

MORTGAGE LOANS

Home ownership is the foundation of the American dream and a top financial goal for many people. But with the median listing price for homes on the market at just over $250,000, according to Zillow, most homebuyers need to finance their purchase with a mortgage instead of paying cash.

Finding the right mortgage loan is arguably just as important as finding the right property. You’ll be paying off your mortgage for years, and the best terms can save you thousands of dollars over time.